10 Predictions About The Future of VC

10 Predictions About The Future of VC

DDVC #68: Where venture capital and data intersect. Every week.

👋 Hi, I’m Andre and welcome to my weekly newsletter, Data-driven VC. Every Thursday I cover hands-on insights into data-driven innovation in venture capital and connect the dots between the latest research, reviews of novel tools and datasets, deep dives into various VC tech stacks, interviews with experts, and the implications for all stakeholders. Follow along to understand how data-driven approaches change the game, why it matters, and what it means for you.

Current subscribers: 17,320, +410 since last week

Brought to you by Gravity - easy-to-use & affordable sourcing tool for data-driven VCs

Gravity tracks exclusive, real-time insights on brand-new startups which allows you to quickly:

Be the first to know when founders leave to start new companies

Know the moment founders go into secrecy or debut their startup out of stealth mode

Discover new startups not found using other data sources

We track billions of data points to help you stay ahead of the fast-moving startup landscape by uncovering startups the moment they hit the web.

VC has long been a cottage industry that has seen little innovation. This is particularly surprising as VCs themselves are the ones backing the most disruptive businesses. They have a front-row seat when it comes to the adoption of new technologies and business model innovation, yet in the first 60 years following the industry’s inception in the 1950s, the only change was the shift from pen & paper to computer & MS Office.

The reason for this lack of innovation is most likely the absence of competition and pressure to change. Access to capital for startups with less traditional business models and a lack of collaterals has historically been heavily constrained. This is why the VC industry evolved in the first place and, unfortunately, this reality is still true for the majority of new startups today.

As a result of a supply-side constrained market, VCs could long afford to be picky and weren’t forced to innovate. Until the early 2010s. Maturing ecosystems and cheap money policy increased new firm formation but also the assets under management per firm. Access to capital became gradually more available for startups and the shift from a supply-side constrained market to a more balanced, partially in 2020 and 2021 even demand-side constrained market, suddenly forced investors to get their act together.

Ever since I joined the VC industry in 2017, I’ve been observing, pushing, and writing about growing innovation in this rusty industry. In today’s episode, I’d like to zoom out again and look at the major trends and predictions for 2024 and beyond. Let’s dive in!

#1 Natural Selection: VCs Cut Headcount, Close Shop & Pursue M&A😵🤝

The VC industry faces a range of challenges. Overpriced portfolio companies, lack of exit channels, DPI and performance issues, fundraising struggles, generational transition, diversity, you name it.

In the past decade, the VC market has seen only one direction: up and to the right. Following 2022, however, this has suddenly changed and I expect a natural selection in the next year or two.

Looking at the drivers of this prediction, I’d like to double-click on the most dominant market-related components.

Venture returns are power-law distributed. Few outsized winners deliver the majority of returns. For this logic to work, VCs need exit channels like IPOs and M&A with significant liquidity.

Deflating public markets end of 2022 and the resulting liquidity crunch were anything but helpful. Since then, many VCs have sat on piles of paper money but cannot divest and deliver DPI.

This translates directly to LPs which in turn have limited resources for new engagements and re-ups. Consequently, their deployment strategy for 2023 and at least until the re-opening of IPO windows towards the end of 2024 or even early 2025 is extremely selective.

“The $67bn raised by US VCs in 2023 is the lowest annual total since 2017 and represents a 60 per cent drop from the $173bn raised in 2022, the peak year for fundraising, according to analysis by private markets data provider PitchBook and the National Venture Capital Association. Globally, in 2023 venture investors raised the lowest level of capital since 2015” (source FT Jan 5 2024)

Based on feedback from various institutional LPs, most of them cut back on new engagements with emerging managers and become hyper-focused on performance KPIs for 3rd generation+ GPs.

Second fund generations are a bit of a different breed as they tend to follow the inaugural fund about 3 to 4 years later and are unlikely to deliver tangible performance that soon. Thus, whenever LPs invest in first fund generations, they typically subscribe (at least in their mind) to the second generation too.

“LPs are aware that when the second fund comes along, they won’t yet know how well the first fund has performed,” says Jeremy Uzan. “In a way, they already knew that they would back fund one and fund two” (source Singular Fund II Announcement, Dec 14 2023)

I expect several GPs with insufficient exit track records and/or other challenges to disappear in the next year or two.

This will most likely hit firms that were founded in the rising market of 2010-2018ish, as they’re old enough for LPs to require KPIs (raising 3rd generation+) but too young to have distributed tangible money to their LPs. Hereof, they either cut headcount to extend runway into hopefully more friendly market environments, close shop, or join forces with other firms.

Though VC as an industry has historically seen very little M&A, recent activities (driven by different motivations, some even from a mutual position of strength, examples above) might provoke a broader appetite for established VC firms to acquire strategic assets like a brand, portfolio, or an investment team from struggling GPs to enter new markets.

#2 Exit Window Will Open End 2024 / Early 2025📈

Our partnership at Earlybird has seen three major downturns since our firm’s inception in 1997: Dotcom, GFC, and COVID. Based on first-hand experience and internal analyses, we find that the private venture capital cycle can be split into 4 major phases.

The full cycle historically took around 5-12 years. Downturn and recovery make up about 3 years of this. Generally, we see that transitions between phases tend to follow a more compressed timeline compared to past cycles.

Below is a chart that we first presented to our LPs in 2022 and so far, the predictions for 2023 have come mostly true. Public markets started recovering, e.g. S&P500 up 26% and NASDAQ up 54% in 2023. At the same time, private venture funding clocks in at the lowest levels in 5 years.

Following this cycle, we expect growing private market investments, and more importantly, exits and distributions again in 2024. The first companies will test the IPO waters likely towards the summer of 2024.

Companies that managed to raise funding throughout 2022-2024 certainly did so because they had clear paths to sustainable growth. The more mature ones among them are waiting to see the IPO window open up again. And they seem to be well-prepared.

Assuming that neither the US elections nor any of the ongoing wars escalate, this momentum might then translate into a strong cohort of VC exits in 2025.

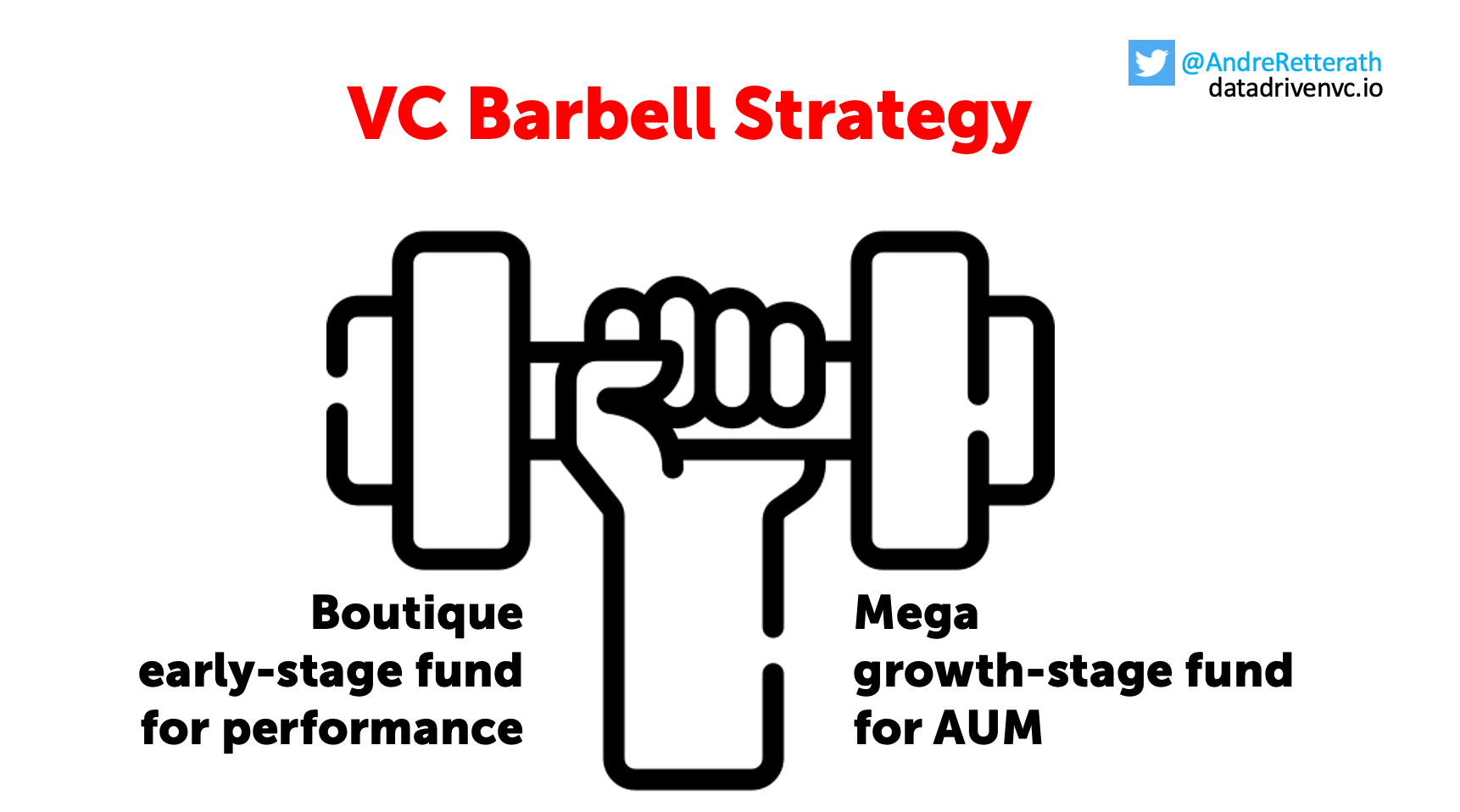

#3 Boutiques, Mega Funds, Barbells, and the VOID🏋️

I predict that three VC models will dominate and the “in-betweens” will disappear.

Boutiques: Exploding capital availability and competition ahead of the boom in 2021 forced VCs to innovate. Solo GPs and micro VCs (<100m) as subforms of boutique firms were a new breed back then but have established themselves quickly.

Recent studies show that smaller funds outperform larger funds and struggle to keep this performance as they grow. Staying small can be a winning model and given the limited size of these funds, it’s easier to raise them compared to larger funds; thus also a feasible model in the current market environment.

In the long term, the option for outstanding performance comes at a cost of limited allocation. Well-performing boutique funds will eventually attract more LP interest, but struggle to stick to their strategy while meeting target allocations. Therefore, boutique firms mostly stick with non-institutional LPs.

Mega Funds: In line with prediction #1 above, established funds that have returned money to their LPs in the past are still able to raise new vintages. Though sometimes (intentionally) smaller or the same size as before, they have historically grown their funds into multi-billion $$.

While larger funds tend to underperform their x-percentile boutique peers, they offer LPs consistent capital allocation with superior returns compared to other asset classes.

Barbell Approach = The Best of Both Worlds: Talking to different GPs about their long-term strategies, the holy grail seems to be a “Barbell” playbook that unifies the best of both worlds:

Start with a boutique-style early-stage fund and keep the size similar over multiple fund generations

Following some SPVs for follow-on rounds, they launch a growth opportunity fund that eventually opens up for investments into non-portfolio companies at later stages to emerge into a proper VC growth fund

Through unique access of the early-stage fund portfolio and strong relationships with anti-portfolio (companies the early-stage fund did not invest in but kept building a relationship with), the growth fund continues to deliver good performance and attracts more institutional LP interest

While bringing the growth fund size into “mega fund” territory and thus increasing AUM and allowing institutional LPs to allocate large amounts of capital, the early-stage strategy stays boutique to deliver outsized returns

Common fund size ratios range between 1:2 to 1:5 for early:growth, whereas the size of the early fund appears to be the limiting factor as performance diminishes

Management fees from the growth fund can be leveraged to invest into a firm-wide platform and indirectly cross-finance the ability to win for the early-stage fund. A nice flywheel of outperformance and institutional capital allocation starts spinning. Some firms even multiply their early-stage strategies and launch standalone partnerships focused on different geographies or industries

The VOID: Having highlighted boutiques, mega funds, and barbell approaches as winning strategies for the years to come, I’m also convinced that the funds in-between will disappear. The funds that started small and grew but neither became an established mega fund nor created a barbell platform will die as they’re too big to deliver outsized performance (compared to boutiques) and too small to attract large institutional investments (compared to mega funds).

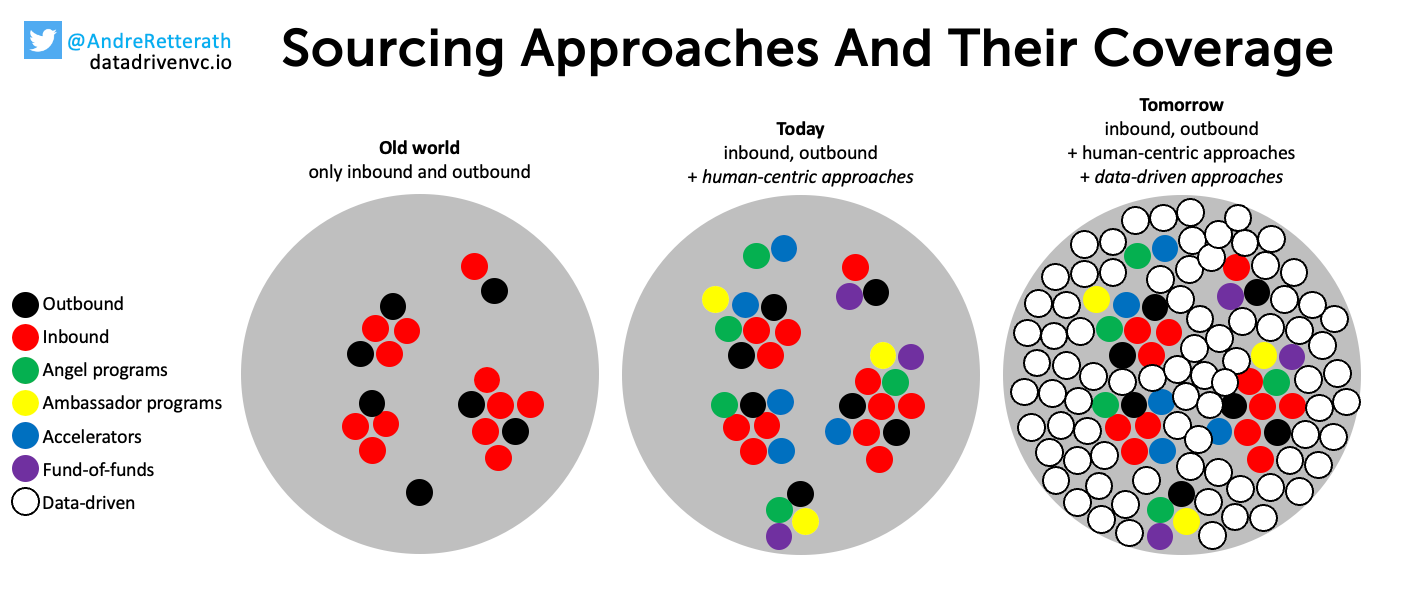

#4 “Preferred” Access to Deals Becomes Key🕵️♂️

One artifact of the competitive market in 2020 and 2021 is the insight that preferred access to deals is key but extremely difficult to achieve. I wrote about different sourcing approaches and their impact on deal coverage here in 2022.

I expect that we’ll continue to see novel and effective approaches, yet once they’ve proven successful, most will be copied by other firms, just like angel or ambassador programs before. Data-driven strategies seem to be the most defensible; more on this below at #6.

On that note, an interesting trend seems to be dedicated fund pockets allocated as a fund-of-fund strategy for upstream funds (that invest earlier). For example, a 500m SerA fund might dedicate 50m to 5 different Pre-Seed and Seed funds with 10m each to get visibility into their portfolio and potentially pre-empt follow-on funding rounds.

Depending on the weight of the investment (e.g. 10m ticket might be an anchor for a Solo GP of 30m; thus extremely important), firms might even discuss preferred participation rights, i.e. handing over pro-rata rights. Don’t want to drop names here, but I know several funds that have such strategic partnerships going on already.

I predict we’ll see more of these innovative concepts as access to deals continues to be core.

#5 2024 Will Be the Year of Pre-Emptions🏃♂️

In line with the previous prediction, it’s not only sufficient to get in front of the most promising entrepreneurs first but also to pull the trigger at the right point in time. In today’s market, this oftentimes means “pre-empting”. Another artifact that lasted from the hype of 2021 (at least in Europe; in the US it seems common practice for longer already).

While historically investors were able to wait for great companies to run a structured fundraising process, to then conduct proper due diligence, decide in their IC, issue a term sheet, and then compete head-on-head with other VC firms, today’s market is different. The best startups rarely run a structured process, they get increasingly pre-empted.

Just in the first ten days of this year, I heard about 3 different European funding rounds that got pre-empted by other funds right before or after Xmas. FOMO is real and I predict 2024 will be the year of pre-emptions.

#6 Massive Disruption Through Data & AI🤖

“We’ve tried this before”, they said. Data-driven approaches in venture are indeed not new. First firms tried to incorporate big data in their investment processes more than a decade ago. Back then, however, they lacked the coverage of private company data as well as the right algorithms. Nice try, but bad marketing timing, I guess.

Today, we have all the ingredients at hand for a perfect storm: Large-scale computing, broad availability of private company data, and intelligent algorithms. When I first embarked on my VC journey in 2017, it took a while to find people in the trenches actually doing what I thought was the right thing to do: leveraging data & AI in VC.

Until 2022, this group of data-driven VCs didn’t grow too much. We kept bouncing ideas, trying different stuff, and oftentimes learned the hard way, how difficult it was to change VC with data & AI.

Through the launch of ChatGPT in November 2022 and generative AI as a trend more broadly, however, things suddenly accelerated. A lot. I know this is true because I’ve been writing and talking about this topic for several years and the number of related inbound requests that I’ve been receiving in the past year is a different game.

In 2024, I see our industry moving from attention and interest to desire and action (AIDA ;)) The VC industry finally becomes more data-driven🥳

#7 Build: Relative Share of Internal (Data) Engineers Increases👩🏽💻

The monthly DDVC wrap-up episodes include job openings for tech positions in VC firms. For comparison, Oct/Nov/Dec wrap-ups 2022 vs 2023 had 2/1/3 vs 11/12/10 job postings. This is on average 5x more positions 2023 vs 2022.

As part of the “Data-driven VC Landscape 2023”, we looked at the 1% of VC firms with internal engineering teams and found that established firms had on average less than 10% engineers. More interestingly, a new breed of firms has been evolving with about 1/3 of internal engineers, representing “AI-first VCs” such as Moonfire (check out my interview with Mike Arpaia here).

Recently, we’ve started our work for the Data-driven VC Landscape 2024 and initial data is incredibly promising: More firms with internal engineering teams and an overall higher percentage of engineers per firm. Get ready for the report towards April/May.

Job postings and insights on changing team compositions. Two data points indicating that engineers become crucial for VC firms.

#8 Buy: “Investment Tech” on the Rise⚒️

There’s hope for those firms unable to afford internal engineering teams. “Investment Tech” is a new category of tools for VC investors to become more efficient, effective, and inclusive - off-the-shelf.

I wrote about make vs buy in the past, and while it might become more difficult (though not impossible!) to generate alpha from these tools vs in-house tech stacks, it allows these firms to get a seat at the table at least.

Thanks to our trusted DDVC community, I know that some high-profile founders are working in stealth to bring AI, agents, and a lot more to VCs who cannot afford to develop their own stack. This comes in addition to existing data, signal, due diligence, or CRM providers launching new AI features. 2024 will be wild.

“Investment Tech” is on the rise and I’ll make sure to cover the most exciting tools in this newsletter.

#9 Fewer Investors Get More Done💪🏼

Through the adoption of data-driven approaches and AI in VC, investors will - as all other knowledge workers too - be able to get more done with less. Investment firms have grown large bodies of analysts and associates to track the markets, keep an eye on promising opportunities, conduct due diligence, and handle transactions.

In a future where intelligent tools free up time for investors to spend their time with more valuable tasks such as founder interactions or actual decision-making, less capacity will be required for monkey work, shifting data and documents from A to B.

As a result, I expect that VC firms longterm reduce investor headcount with a focus on quality decision-making and an ability to win competitive deals.

#10 Reputation & Brand Become Key🏆

“As the VC industry becomes more efficient, two “access components” will become core: capital availability (which VC is able to pay the highest valuation) and VC brand (firm brand + personal brand of the individual investor) — besides personal fit (which will remain key)”

The quote above is from my 2020 “The Future of VC: Augmenting Humans with AI” and I can’t repeat it often enough: Brand is a key factor to win competitive deals. It has two dimensions: The firm brand and the personal brand of the individual deal makers.

I wrote about “Why you need a strong firm and personal brand” and “Personal Branding 101” before as these are among the few factors in the long-term oriented VC world that one can influence short- and midterm.

Firm E has the best brand, closely followed by firm C. An investor with a great personal brand in firm C is likely to win a deal against a relatively worse investor at firm E. This logic summarizes one core aspect: VC firms are partnerships of individual human beings. Our collective personal brands make up the firm brand.

Overrated: Being well-known.

Underrated: Being known well.

In a time when cash has become a commodity and the best founders can pick their investors, a reliable, trusted VC brand is key. 2024 will be a year of interesting brand initiatives.

Conclusion

Though the VC industry had a tough time in 2023, I’m overall incredibly positive and excited for 2024 and beyond. I will make sure to track & write about the most important dynamics in this newsletter. Let’s see if and when my predictions come true.

What are your predictions? Do you agree, disagree, or have something to add? Like and leave a comment below :)

Stay driven,

Andre

Thank you for reading. If you liked it, share it with your friends, colleagues, and everyone interested in data-driven innovation. Subscribe below and follow me on LinkedIn or Twitter to never miss data-driven VC updates again.

What do you think about my weekly Newsletter? Love it | It's great | Good | Okay-ish | Stop it

If you have any suggestions, want me to feature an article, research, your tech stack or list a job, hit me up! I would love to include it in my next edition😎